Nevertheless, once the prepaid rent has been used up, exhausted, or expired, the expense is recorded on the income statement. The difference between the actual cash rent payments and the straight-line rent expense is recorded as deferred rent on the balance sheet. To determine whether prepaid rent is an asset, we must first consider whether it meets the definition of an asset. Prepaid rent has economic value, representing a payment made in advance for using a property. It also provides future benefits, as the landlord will apply the charge towards the upcoming rental period or periods.

Prepaid Rent Under ASC 842 – a Step-By-Step Guide & Example

When looking at the definition of an asset, recall that an asset is considered to be something that provides a current, future, or potential economic benefit for an individual or company. It is something that is owned by the company or something that is owed to the company. This is because prepaid rent provides a future economic benefit to the company by reducing rent expenses when incurred. The company can make the prepaid rent journal entry by debiting the prepaid rent account and crediting the cash account after making the advance payment for the rent of facility.

Step 3: Calculate the operating lease liability

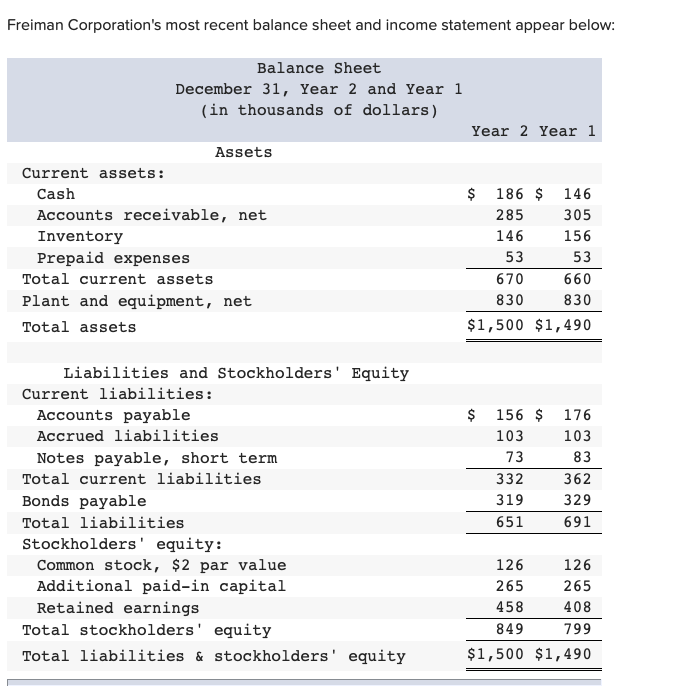

When cash payments in a period were less than the expense incurred, deferred rent would be recognized on the balance sheet as a credit balance. This was considered a deferral, which is a liability, as expense for rent was incurred, but some of the amount was still owed. For further explanation of deferred rent, see our blog, Deferred Rent under ASC 842 Explained with Examples and Journal Entries. A current asset account that reports the amount of future rent expense that was paid in advance of the rental period. The amount reported on the balance sheet is the amount that has not yet been used or expired as of the balance sheet date. When prepaid rent is paid, it increases the current assets on the tenant’s balance sheet.

Is Prepaid Rent Debit or Credit?

In short, store a prepaid rent payment on the balance sheet as an asset until the month when the company is actually using the facility to which the rent relates, and then charge it to expense. If the company classifies expenses into administrative and selling expenses, rent expense should be apportioned based on the space used by the administrative department and the selling department. The amount of prepaid rent is reported on the balance sheet of a business renting a property as a current asset account that will be expensed at some point in the future. Therefore, until the amount of prepayment is actually used up in payment for a month’s use of the leased property, it must be properly recorded as a current asset on the company’s balance sheet.

What is the best way to estimate the amount of a prepaid asset’s monthly benefit?

We then add the prepaid amount of $36,721 to establish the Right-of-use (ROU) Asset balance, which comes out to be $101,749. In essence, there is no such account named “prepaid rent” on the balance sheet under the rules of ASC 842. Instead, such an asset is recognized as part of the Right-of-use (ROU) Asset balance.

Prepaid Rent Accounting

- According to generally accepted accounting principles (GAAP), expenses should be recorded in the same accounting period as the benefit generated from the related asset.

- Current assets are assets that a company plans to use or sell within a year; they are short-term assets.

- This lesson explains when prepaid expenses are incurred and offers examples of common prepaid expenses.

- Prepaid rent is rent that’s been paid in advance of the period for which it’s due.

- The systematic reduction of the prepaid rent asset is crucial in matching expenses with the periods in which they are incurred, adhering to the matching principle of accounting.

Likewise, the journal entry here doesn’t involve an income statement account as both prepaid rent and cash are balance sheet items. Hence, the journal entry above is simply increasing one asset (prepaid rent) together with the decreasing of another asset (cash). By applying the present value (PV) formula or a PV calculator, the PV of the remaining payments is determined to be $65,028. It is important to note that in this calculation, the first period is accounted as ‘zero’ in the annuity/cash flow. This is because it has already been prepaid and is not included in the lease liability. Additionally, at the time of transition to ASC 842, any outstanding prepaid rent amounts would be included in the calculation of the appropriate ROU asset.

Both rent expense and lease expense represent the periodic payment made for the use of the underlying asset. Organizations may have a commercial leasing arrangement or a rental agreement. In the balance sheet, all the prepaid expenses that have not yet been consumed are recorded as current assets.

Current assets are the assets that a business owns and expects to realize within 12 months or the operating cycle. Some examples of current assets are Bills Receivables, Cash, Cash at Bank, Inventories, etc. Prepaid assets represent prepaid rent assets or liabilities the right to receive future services, while deferred revenue represents the right to receive future cash payments. Therefore, as the benefits of the prepaid rent are realized, it is recorded on the income statement.

However, whether you classify prepaid rent as a current or long-term asset depends on the length of the lease term. If the lease term is less than one year, consider this a current investment because you expect it to be used or converted into cash within one year. Further details on the treatment of pre paid rent can be found in our prepaid expenses tutorial. At the end of April one third of the prepaid rent expense (1,000) will have been used up as the business has used the premises for that month.

By correctly differentiating between prepaid rent and rent expense, businesses can accurately report their financial position and ensure the integrity of their financial statements. The long-term assets or non-current assets include the items and resources that cannot be quickly converted into cash. Non-current assets (long-term) and current assets (short-term) are categories of assets owned by an entity.

0 comments